How can I buy a property with no savings?

I bought this property in Apr 2019, the problem I had was

What does this have to do with you?

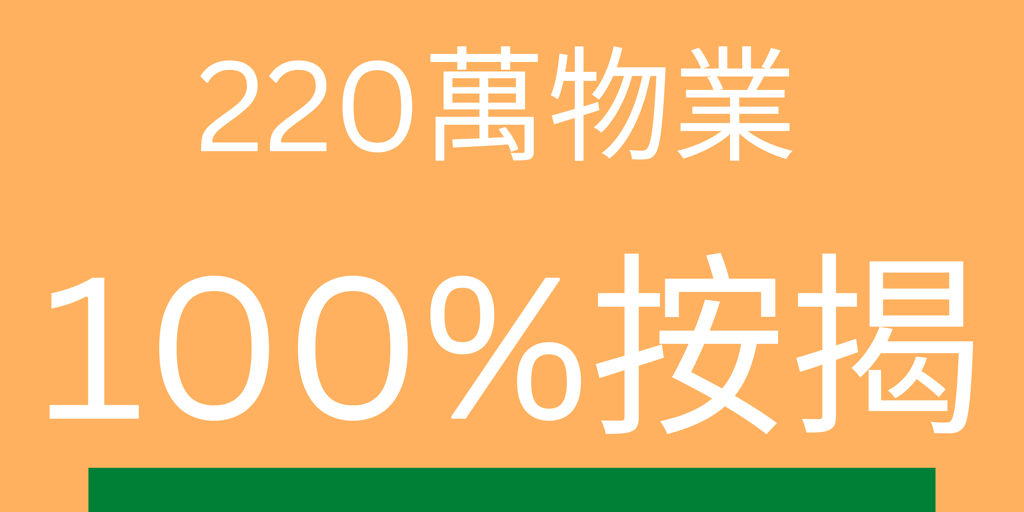

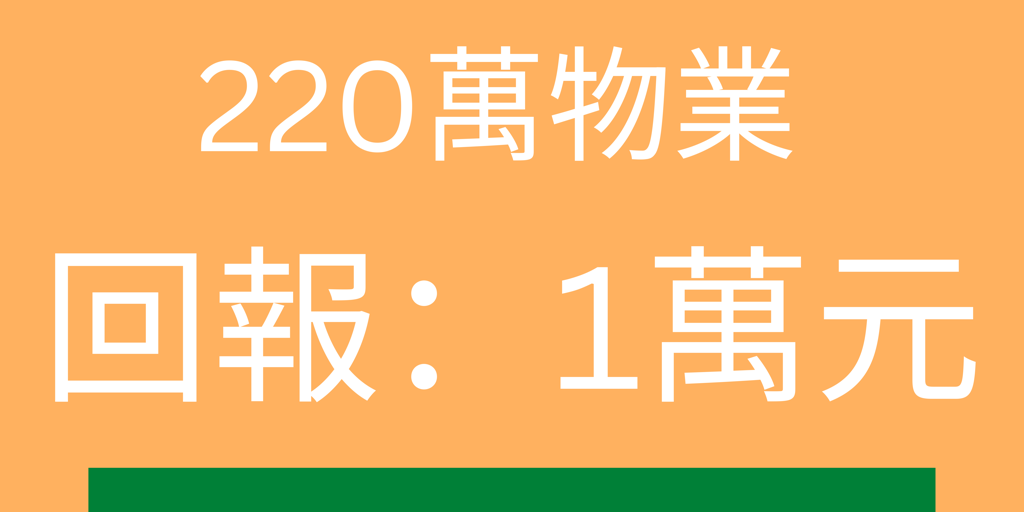

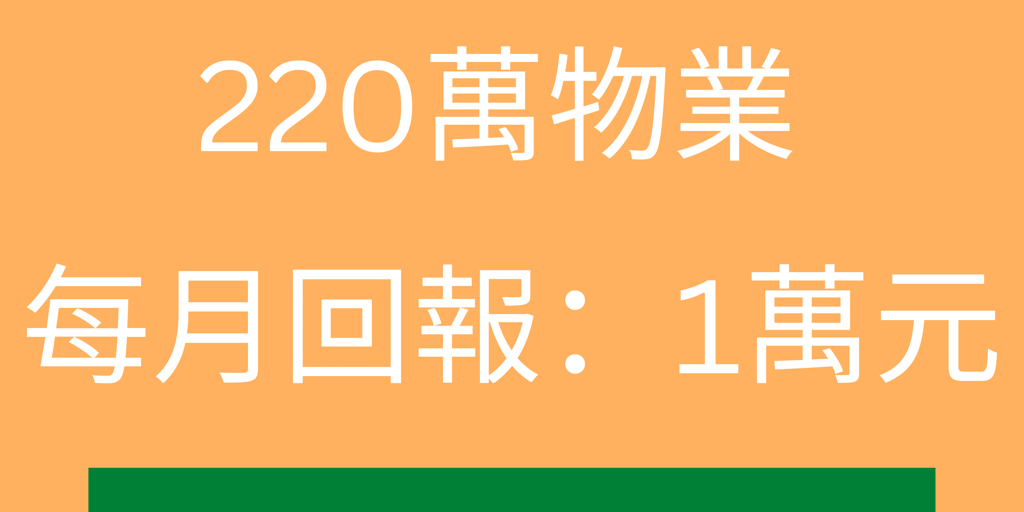

I like to take you through step by step: Step 1 This was what I did. We have our first house purchased in 2008 at 1.95mil. Maybe you don’t have a property. Please read on because maybe your parents do, you just need to do the right calculations. I apply for a remortgage with that first house so that to pay for the downpayment. What you have to do You need to know if your parent can remortgage their house so you can make a downpayment and know how much it cost them. You promise to pay them back. You can use different mortgage calculator to know the monthly payment. Step 2 Then, I apply for remortgage to get 1.4 mil for my first house. The monthly repayment is 4768. So 1.4mil= 4768 monthly repayment What you have to do Keep this remortgage figure in mind because you will pay back parents or I m in trouble 🙀 Step 3 Then, I apply for another mortgage for my second house. Purchase Price 2.2 mil x 60%, so I get another 1.32 mil mortgage. Monthly payment is 5710. What you have to do Find any property to do a calculation. To determine your price range for me. I target 2 mil to 3 mil on my second property. The best case scenario is you can find a property that the rent cover both parent’s mortgage plus your new mortgage. This isn’t easy you need to search. Step 4 For my second house, this is the calculation Total mortgage is 1.4 mil + 1.32 mil = 2.72 mil. My property prices is 2.2 mil. I have 0.52 mil on hand. Total repayment is 4768+ 5710= 10478 per month I was able to collect a rent of 9300. I need to pay 10478- 9300 = 1178 per month to own my 2.2 mil house. Plus, I got cash 0.52mil cash on hand. What Rich Dad Taught Me Best case scenario “Rent > Mortgage” As taught by Rich Dad, your should produce a cashflow that is greater than your mortgage. That is your rent is high enough to cover your mortgage and other expenses that allows you to generate income from the property. Go to my website www.dadDAYout.com to find out more

0 Comments

Leave a Reply. |

Motivation BlogA project about being a property entrepreneur and motivation speaker. How I work from a job transforming into a business. I went through 3 business failures, broken relationship and on Apr 24, 2019. I invested my first property with 100% mortgage Archives

November 2022

Categories

All

|

RSS Feed

RSS Feed

Proudly powered by Weebly